Three interesting charts, two of which are from Dough Wakefield:

This chart looks rather scary. If companies ran into troubles in 2001/01 and 2008/09 but survived, then their valuations should be relatively cheaper now. But if companies did go bankrupt, then value was destroyed permanently for investors in those companies.

I am less negative than the writer of the article, shares are probably in general somewhat expensive, but not overvalued as much as in 2000 or 2007.

The above chart shows that high yield bonds also went up a lot. The article therefore poses the question:

"Straightforward analysis of these two charts happens to fire a torpedo into the current thesis that we should all be preparing for some kind of ‘Great Rotation’ out of bonds and into stocks. What are we all supposed to do if stocks and (in this case, high yield) bonds are both expensive?"

And another, intriguing question:

“Is it possible that the big banks, after never having more than $60 billion in excess reserves between 1957 (oldest date I could find on a Federal Reserve website) and the end of 2008, are sitting on more than $1.5 trillion at the end of 2012 because they are preparing for a massive DEFLATION of asset prices in the future ? What about big corporations, who recently reached their largest amount of cash on record ?”

That sounds indeed puzzling.

Another observation by the writer:

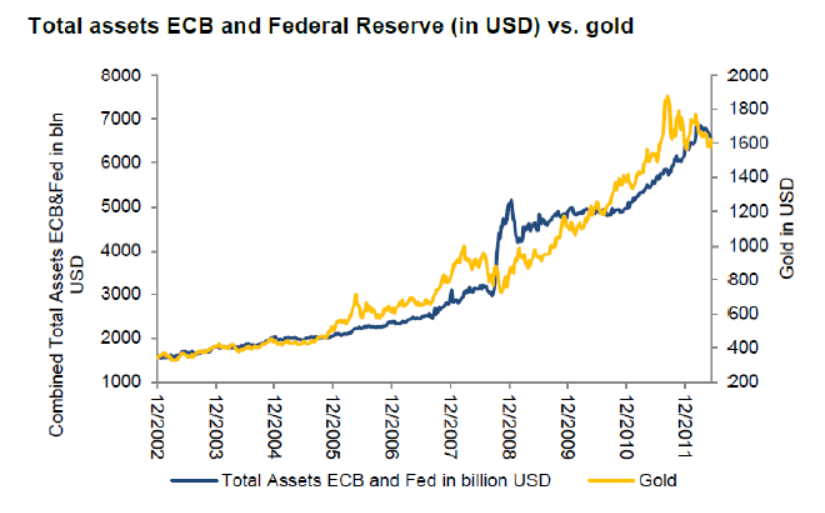

We note that Credit Suisse has now run up the white flag on gold, declaring that the precious metal “appears significantly overvalued”. By comparison to what, exactly ? Or as expressed in what, exactly ? We think Credit Suisse’s gold analysts understand as much about gold as Kermit the Frog or any other of the Muppets. The chart below, for example, shows the extent to which central banks have recently inflated their balance sheets:

Indeed, a remarkable correlation. The kind of chart that reminds me that countries that report extraordinary low inflation of 1% or 2% (Malaysia is one of those, but there are many others) might significantly under-report the real numbers.

And the last observation of Tim Price:

"So while we can state with a high degree of certainty that this mess really will end badly, we can’t state with any certainty over what time period it does so. So we are quite content to shelter in a variety of sensibly selected and genuinely disparate asset classes, and meanwhile pick fights with any and all comers who seem to have grave difficulty in distinguishing between nominal price returns and substantive, lasting value. Pay your “money”, and take your choice."

No comments:

Post a Comment