"Iceberg Research", an unknown and anonymous website, has issued a

negative report about Noble Group, the commodity trading company listed on the SGX.

For me, the most important is if the allegations are true and the most interesting item is the valuation of Yancoal in Noble's books:

- Noble owns 13% of their shares;

- Yancoal is listed and the 13% of the market cap is worth about $11M;

- Yet the investment is in the books of Noble for $614M;

- Noble doesn't seem to have significant control over the company.

That looks very weird, to put it mildly.

Macquarie

writes:

"But the shares are thinly traded, which can distort market value. This is one reason why Noble can use a financial model, reviewed by auditors Ernst & Young, to value the stake. With sustained weak coal prices, we have been flagging the risk of further write downs for YAL (2012 carrying value: US$813m). The Noble CEO himself hinted at such a potential outcome at a recent sell side event. Whilst we do not see the full carrying value at risk, there could be a non-trivial impact vis-à-vis Noble’s S$0.98 BVPS (excluding perpetuals). But, again, we have been flagging this risk for well over a year."

Regular readers of this blog will know what I think about the many financial calculations (most of them DCF models) that are being used. Changing one single parameter would already later the outcome of the model hugely, but there are often many important parameters. The result is a very wide

range of valuations (not a single valuation), the lowest of which has to be zero.

In other words, giving a single valuation through the use of these kind of models is (in most cases) useless, rubbish and self-serving.

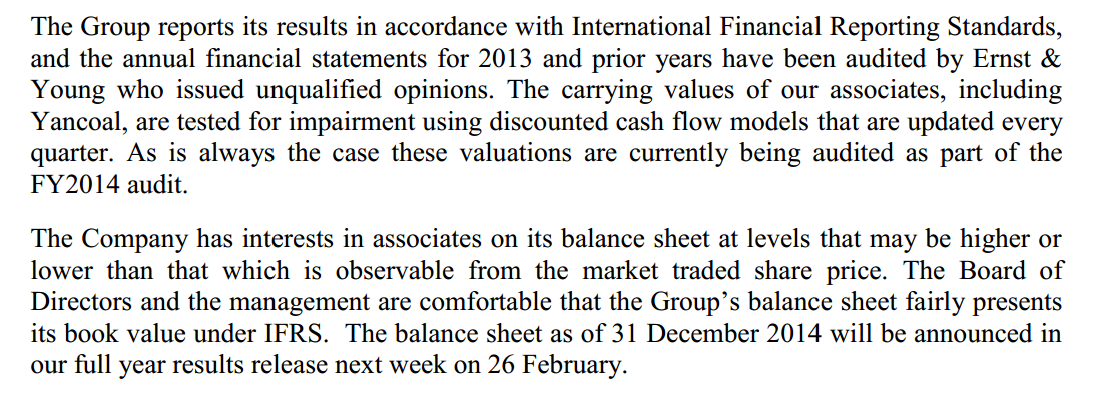

Noble has since

responded, no surprises here:

If the DCF model of the stake in Yancoal does indeed indicate a valuation of $614M, 56 times as much as the current market price, then the company really should publish the model's assumptions and calculations, for all to see. We could then also check the model with the outcome say three years down the road.

Unfortunately, publishing the model's details hardly ever happens is my experience.

The Monetary Authority Singapore (MAS) is looking into the case, Noble's year report will be announced on February 26, 2015.