Article at Bloomberg's website:

Singapore Exchange Takes on Hong Kong With Dual-Class Shares

One snippet:

Singapore Exchange Ltd. said it allow companies with dual-class share structures to list, a month after Hong Kong announced a similar proposal, as competition between markets for technology listings becomes increasingly fierce.

Sigh. I think the SGX is making a mistake here: bending backwards in CG terms and complicating rules and legislations in the hope of getting large IPOs like Facebook or Alibaba to list in Singapore. I don't think that won't happen anyhow (SGX is simply not attractive enough at the moment).

A critical article:

SGX's Doubly Bad Idea

Even in the unlikely event that a company will IPO with dual class shares and the company will be a huge success operationally, the result might be limited. Makers of indices are considering leaving out companies with dual class shares, like the S&P 500:

"Farewell, Snap Inc (NYSE: SNAP), we hardly knew ye." That was the message from the Standard & Poor's 500 index on Tuesday, when it suddenly stopped allowing companies with dual-class share structures to join the index.

That means that most likely ETFs who follow indices on Singaporean, ASEAN, Emerging Markets or Global shares will not include companies listed on the SGX with a dual class structure.

Also, many active fund managers will frown upon these companies due to serious CG concerns.

The result would be that these companies trade at a sizeable discount to comparable companies with one class, and deservedly so.

Singapore has in the past actively encouraged mainland China companies to list on the SGX (the so called S-chips), is recently active in ICOs, soon allowing dual class shares and it might require less companies to issue quarterly reports. From a CG point of view, this all seems (very) worrisome.

What do we get next, a S-chip company with half yearly reporting having a dual class share structure issuing an ICO? The possibilities seem endless. But does this all really benefit the Singaporean economy in the long term? I strongly doubt it.

I have a lot of respect for the long term planning and execution in Singapore for instance regarding infrastructure, it is very impressive. But somehow this does not seem to apply to the financial markets.

Malaysia seems to have things better organized; it does not intend to allow dual class shares and issued a very clear warning regarding ICOs.

Showing posts with label SGX. Show all posts

Showing posts with label SGX. Show all posts

Wednesday, 24 January 2018

Wednesday, 13 September 2017

Raising the bar for SGX delistings

Article in The Straits Times, some snippets:

For a company to be voluntarily delisted, a shareholders' meeting must be held where approval for the move must be received from 75 per cent of the shareholders present and where not more than 10 per cent disagree with the move.

The snag is that this feat is made easier because the listing rules here do not bar directors and major shareholders from voting - and since the major shareholder, usually also the company boss, is the party proposing the delisting move, the odds are stacked heavily against minority shareholders.

In recent years, however, some companies are being taken private at a very low valuation at the bottom of the business cycle, only to be relisted in another jurisdiction at a much higher valuation.

No wonder, some minority shareholders feel existing listing rules fail to give them adequate protection if an opportunistic major shareholder wants to delist the company and attempt to squeeze them out of their shares at unattractive prices.

..... the academics observed that there had been instances of IFAs assessing offers as being "fair and reasonable" even when the exit offer in question was at a steep discount of more than 30 per cent to the latest NAV of the takeover target.

Against this backdrop, I would say that the SGX listing manual is due for an overhaul.

Delistings have become a red-button issue among aggrieved minority shareholders. It is one area that urgently needs to be looked into when the rule book is revamped.

For a company to be voluntarily delisted, a shareholders' meeting must be held where approval for the move must be received from 75 per cent of the shareholders present and where not more than 10 per cent disagree with the move.

The snag is that this feat is made easier because the listing rules here do not bar directors and major shareholders from voting - and since the major shareholder, usually also the company boss, is the party proposing the delisting move, the odds are stacked heavily against minority shareholders.

In recent years, however, some companies are being taken private at a very low valuation at the bottom of the business cycle, only to be relisted in another jurisdiction at a much higher valuation.

No wonder, some minority shareholders feel existing listing rules fail to give them adequate protection if an opportunistic major shareholder wants to delist the company and attempt to squeeze them out of their shares at unattractive prices.

..... the academics observed that there had been instances of IFAs assessing offers as being "fair and reasonable" even when the exit offer in question was at a steep discount of more than 30 per cent to the latest NAV of the takeover target.

Against this backdrop, I would say that the SGX listing manual is due for an overhaul.

Delistings have become a red-button issue among aggrieved minority shareholders. It is one area that urgently needs to be looked into when the rule book is revamped.

The same applies to Bursa, a revamp is needed in which minority investors receive more protection from delistings at a very low price, it is long overdue.

Monday, 3 April 2017

The Shame of Germany's Ship Owners

Article from Handelsblatt Global:

The Shame of Germany's Ship Owners

"No country is more irresponsible when it comes to disposing of its ships than Germany. Even the United Nations is protesting about it."

A snippet:

The list names and shames companies that have their end-of-life ships broken up on beaches in Bangladesh, India and Pakistan. The German ship owners were responsible for the “worst shipbreaking practices amongst all shipping nations,” according to Shipbreaking Platform.

Until now, this has been a taboo topic in Hamburg shipping offices, and for good reason. South Asian beaching yards are notorious for eschewing environmental and safety standards and abusing worker rights. Oil and toxic chemicals seep into the sea. Laborers are exposed to asbestos. Many die in accidents.

Rickmers is mentioned, which manages and majority owns Rickmers Maritime, a business trust listed on the SGX.

The Shame of Germany's Ship Owners

"No country is more irresponsible when it comes to disposing of its ships than Germany. Even the United Nations is protesting about it."

A snippet:

The list names and shames companies that have their end-of-life ships broken up on beaches in Bangladesh, India and Pakistan. The German ship owners were responsible for the “worst shipbreaking practices amongst all shipping nations,” according to Shipbreaking Platform.

Until now, this has been a taboo topic in Hamburg shipping offices, and for good reason. South Asian beaching yards are notorious for eschewing environmental and safety standards and abusing worker rights. Oil and toxic chemicals seep into the sea. Laborers are exposed to asbestos. Many die in accidents.

Rickmers is mentioned, which manages and majority owns Rickmers Maritime, a business trust listed on the SGX.

Thursday, 2 March 2017

Webb on SGX

A link and comments on the website of David Webb:

"They reportedly also propose widening the bid-offer spread, which is a sure-fire way to reduce liquidity, not increase it. This is another sign of desparation after the proposal to list second-class shares. Who is running SGX these days? What next - introducing minimum commissions? Rather than fiddle with trading hours and rules, consider allowing competing exchanges, then let the market discover which hours and spreads it wants."

A previous article by Webb on bid-offer spreads can be found here: HKEx keeps wide spreads

"They reportedly also propose widening the bid-offer spread, which is a sure-fire way to reduce liquidity, not increase it. This is another sign of desparation after the proposal to list second-class shares. Who is running SGX these days? What next - introducing minimum commissions? Rather than fiddle with trading hours and rules, consider allowing competing exchanges, then let the market discover which hours and spreads it wants."

A previous article by Webb on bid-offer spreads can be found here: HKEx keeps wide spreads

Thursday, 23 February 2017

New ETFs: exotic or toxic?

Article on Bloombers website:

Singapore Readies New Exotic ETFs to Catch Taiwan, Hong Kong

A snippet:

Preparations are underway in Singapore for the first new listing of leveraged and inverse exchange-traded funds in almost eight years.

Singapore Exchange Ltd. last week published a new web page about the products, described as “a form of passive collective investment schemes (like ETFs) and structured as open-end funds,” following revised guidelines from the Monetary Authority of Singapore in August.

Singapore, along with Hong Kong, is seeking to capture a bigger share of an expanding pie through types of funds that have seen success in Japan, Taiwan and Korea. Leveraged ETFs in Taiwan, which started in 2014, now have more than $4.8 billion in assets, according to data compiled by Bloomberg. Daily trading of inverse and leveraged funds is more than half of Taiwan’s ETF market, said Andy Chang, president and chief executive officer of Cathay Securities Investment Trust Co.

I am seriously underwhelmed by this initiave, is this really the best the SGX can come up with to attract retail investors?

I like "long" ETFs on a certain large market with low fees very much, I use them myself if I think a market is relatively cheap and I don't have my eyes on some particular stocks in that market.

I can also imagine that an investor sometimes wants to invest in an inverse ETF without leverage, as a (partial) insurance against his portfolio of value shares going down together with the market when the market looks richly priced but the value shares still offer enough upside.

But these leveraged ETFs, I am not keen at all on them, the management fees are often much higher than the "long" only ETFs. In addition to that there are also higher expenses related to the instruments the ETFs use to create the leverage. In the longer term the fees will have a serious impact on the returns.

Singapore Readies New Exotic ETFs to Catch Taiwan, Hong Kong

A snippet:

Preparations are underway in Singapore for the first new listing of leveraged and inverse exchange-traded funds in almost eight years.

Singapore Exchange Ltd. last week published a new web page about the products, described as “a form of passive collective investment schemes (like ETFs) and structured as open-end funds,” following revised guidelines from the Monetary Authority of Singapore in August.

Singapore, along with Hong Kong, is seeking to capture a bigger share of an expanding pie through types of funds that have seen success in Japan, Taiwan and Korea. Leveraged ETFs in Taiwan, which started in 2014, now have more than $4.8 billion in assets, according to data compiled by Bloomberg. Daily trading of inverse and leveraged funds is more than half of Taiwan’s ETF market, said Andy Chang, president and chief executive officer of Cathay Securities Investment Trust Co.

I am seriously underwhelmed by this initiave, is this really the best the SGX can come up with to attract retail investors?

I like "long" ETFs on a certain large market with low fees very much, I use them myself if I think a market is relatively cheap and I don't have my eyes on some particular stocks in that market.

I can also imagine that an investor sometimes wants to invest in an inverse ETF without leverage, as a (partial) insurance against his portfolio of value shares going down together with the market when the market looks richly priced but the value shares still offer enough upside.

But these leveraged ETFs, I am not keen at all on them, the management fees are often much higher than the "long" only ETFs. In addition to that there are also higher expenses related to the instruments the ETFs use to create the leverage. In the longer term the fees will have a serious impact on the returns.

Thursday, 22 December 2016

It's a small world

Two interesting articles:

Penny stock crash: John Soh accused of witness tampering

7 executives of Platinum Partners charged with US$1 bil fraud

Penny stock crash: John Soh accused of witness tampering

7 executives of Platinum Partners charged with US$1 bil fraud

In it the companies in the "Penny Stock Saga" (Blumont, Asiasons and LionGold) are linked to ISR and John Soh and to US-based hedge fund Platinum Partners.

It is indeed a small world in the world of finance.

Good to see that at least some enforcement is being delivered in Singapore and the US.

Remains the question: John Soh seems to be (allegedly) the mastermind in this all, what would have happened if the Malaysian authorities would have punished him more appropriately for his alleged role in the downfall of several Malaysian listed companies?

The fine of RM 6 Million seems to be woefully inadequate, at least to me.

Sunday, 27 November 2016

Chinese "IPO fraud school"

Interesting article on Seeking Alpha:

KGJI: A 'Fraud School' Success Story

Muddy Waters, a research firm that has exposed many Chinese frauds, authored a White Paper on the organized network that brought numerous fraudulent companies onto U.S. exchanges. The presentation and research paper, Frauducation, cited a 2012 Chinese Today's Fortune article that discussed an investigation into a Chinese "fraud school." The article (translated into english) describes a "systematically criminal" platform:

... the "fraud school" is a small investment bank and financing counseling company. It uses a network of accounting firms and law firms based in HK and US to jointly operate to present "trash" enterprises as fast-growing and huge-profitmaking super stars, thus catching the foreign investors' eyes, gaining private funding, and subsequently going public in the US....After that, they will keep coaching the firm on producing falsified reporting documents in order to make it keep "growing" with the eventual goal of listing on a primary exchange (i.e. NYSE or NASDAQ) and collect even more money from US investors.

While the investment bank leading the fraud school was not specifically named in the article, the research paper highlighted the likelihood of it being a Hong Kong outfit named Chief Capital.

The Frauducation white paper also examined the audit firm of Jimmy C.H. Cheung & Company. Cheung was the earliest auditor of record for RINO and audited ChinaCast (OTCPK:CAST) which, according the SEC, was a "massive" fraud. We discovered that Cheung also performed audit work for Kingold.

The article further details alleged irregularities regarding Kingold. The share of Kingold went down from 2.00 to about 1.30, but recovered to 1.60 on Friday.

A video by Muddy Waters about the alleged Chinese fraud school can be found here.

I am not aware if any Bursa or SGX listed company went to this alleged fraud school. But the audit firm of Jimmy C.H. Cheung & Company (featured in the above video) did auditing work for a SGX listed company.

The firm is called International Healthway Corp (IHC), from it's IPO offer document (dated 1 July 2013)

And it seems that nothing has changed, the same auditor is still auditing the subsidiaries in Hong Kong according the the latest anual report. That looks like a red flag.

But there are many more red flags. Investor Central in an article named "International Healthway Corporation Limited - Do the directors really live in the Thye Hong industrial building in Leng Kee?" came up with "29 questions that need to be asked".

And according to this article the authorities are also looking at trading of IHCs shares.

Even in the boardroom there seems to be problems.

The auditor of IHC (PricewaterhouseCoopers) issued a "disclaimer of opinion" in the 2015 annual report:

KGJI: A 'Fraud School' Success Story

Muddy Waters, a research firm that has exposed many Chinese frauds, authored a White Paper on the organized network that brought numerous fraudulent companies onto U.S. exchanges. The presentation and research paper, Frauducation, cited a 2012 Chinese Today's Fortune article that discussed an investigation into a Chinese "fraud school." The article (translated into english) describes a "systematically criminal" platform:

... the "fraud school" is a small investment bank and financing counseling company. It uses a network of accounting firms and law firms based in HK and US to jointly operate to present "trash" enterprises as fast-growing and huge-profitmaking super stars, thus catching the foreign investors' eyes, gaining private funding, and subsequently going public in the US....After that, they will keep coaching the firm on producing falsified reporting documents in order to make it keep "growing" with the eventual goal of listing on a primary exchange (i.e. NYSE or NASDAQ) and collect even more money from US investors.

While the investment bank leading the fraud school was not specifically named in the article, the research paper highlighted the likelihood of it being a Hong Kong outfit named Chief Capital.

The Frauducation white paper also examined the audit firm of Jimmy C.H. Cheung & Company. Cheung was the earliest auditor of record for RINO and audited ChinaCast (OTCPK:CAST) which, according the SEC, was a "massive" fraud. We discovered that Cheung also performed audit work for Kingold.

The article further details alleged irregularities regarding Kingold. The share of Kingold went down from 2.00 to about 1.30, but recovered to 1.60 on Friday.

A video by Muddy Waters about the alleged Chinese fraud school can be found here.

I am not aware if any Bursa or SGX listed company went to this alleged fraud school. But the audit firm of Jimmy C.H. Cheung & Company (featured in the above video) did auditing work for a SGX listed company.

The firm is called International Healthway Corp (IHC), from it's IPO offer document (dated 1 July 2013)

And it seems that nothing has changed, the same auditor is still auditing the subsidiaries in Hong Kong according the the latest anual report. That looks like a red flag.

But there are many more red flags. Investor Central in an article named "International Healthway Corporation Limited - Do the directors really live in the Thye Hong industrial building in Leng Kee?" came up with "29 questions that need to be asked".

And according to this article the authorities are also looking at trading of IHCs shares.

Even in the boardroom there seems to be problems.

The auditor of IHC (PricewaterhouseCoopers) issued a "disclaimer of opinion" in the 2015 annual report:

Saturday, 8 October 2016

Idea: Tracker Fund of Hong Kong (2800.HK) (2)

I posted about 3 months ago the first investment idea.

This first idea has performed quite well, from HKD 20.90 to currently HKD 24.60, a gain of about 18%.

I expect a decent dividend to be announced at the end of this month (accompanied by a drop in share price of the same amount).

CLSA published their "Asia Maxima" 4Q16 publication:

Interesting are both the low PB and high dividend yields for Hong Kong, which were indeed reasons for me to buy into the Tracker Fund. I am not too worried about the low earnings growth and ROE, I think they are quite typical for a share market when the economy is not doing well. When the economy swings back to live, these factors will undoubtedly improve.

Singapore's numbers are quite similar to those from Hong Kong.

For Malaysia, as usual, quite high PE numbers. But in the stock universe of CLSA (consisting probably of both higher quality and more liquid shares than average) they do predict a positive earnings growth. That is quite different from the overall picture of the 30 largest cap shares on Bursa where an earnings decline is likely. For me the value in Malaysia has always been in selected small and medium cap shares, not in the blue chips.

In general, emerging markets look cheap relatively versus for instance the US market, which is close to its all-time high and which hasn't seen a bear market since 2008/9.

This first idea has performed quite well, from HKD 20.90 to currently HKD 24.60, a gain of about 18%.

I expect a decent dividend to be announced at the end of this month (accompanied by a drop in share price of the same amount).

CLSA published their "Asia Maxima" 4Q16 publication:

Interesting are both the low PB and high dividend yields for Hong Kong, which were indeed reasons for me to buy into the Tracker Fund. I am not too worried about the low earnings growth and ROE, I think they are quite typical for a share market when the economy is not doing well. When the economy swings back to live, these factors will undoubtedly improve.

Singapore's numbers are quite similar to those from Hong Kong.

For Malaysia, as usual, quite high PE numbers. But in the stock universe of CLSA (consisting probably of both higher quality and more liquid shares than average) they do predict a positive earnings growth. That is quite different from the overall picture of the 30 largest cap shares on Bursa where an earnings decline is likely. For me the value in Malaysia has always been in selected small and medium cap shares, not in the blue chips.

In general, emerging markets look cheap relatively versus for instance the US market, which is close to its all-time high and which hasn't seen a bear market since 2008/9.

Sunday, 11 September 2016

Dual class shares: another really bad idea

Both the SGX and Bursa seem to contemplate allowing companies to list with a dual class share structure. That sounds like a really bad idea.

Luckily quite a few parties have spoken out against it, for instance:

Luckily quite a few parties have spoken out against it, for instance:

- Business Times

- Mak Yuen Teen

- MSWG ("is Malaysia ready for dual-class shares" in The Edge Malaysia)

- Abderdeen

David Webb wrote about the same issues in the Hong Kong context.

The arguments in favour of a single class of shares are rather obvious: a simple, clear structure, which has been proven in time. With enforcement that is not "that great", a lack of shareholders activism in both countries, at least (in some rare cases), minority shareholders do have a chance.

What are the arguments of the people supporting a dual class share structure? They are often rather "vague", for instance:

- "The envisaged dual-class share structure listing framework is intended to enhance SGX’s attractiveness as a listing venue and to broaden and deepen Singapore’s capital market" (article)

- "This is about SGX and the Singapore authorities realising that tech companies need a space where they are safe and able to grow, at every stage of their development" (article)

- "The approval of the dual-class share structure in Singapore has shown our Garden City to be a progressive financial hub and might help bring in more listings here in the future." (article)

- ".... founders of companies often have a longer term vision in mind compared to investors who tend to be more focused on short-term gains. The structure hence, protects the founders against short-term pressure for returns" (article)

The argument about tech companies is really strange. Most tech companies will raise money from VC (Venture Capital) firms before they list on an exchange. The VCs will invest their money in exchange for shares, not the normal shares, but (rather ironically) preferred shares which will have much more rights attached than the founders, not less.

For instance they are entitled to a "liquidation preference", besides that they often have a veto right over corporate restructuring, sometimes they even have the right to fire the founders and/or push a deal through which they like and the fouders not.

Founders still accept those deals, because the money is good. So much for the "short-term pressure for returns" argument.

The other argument about attracting companies from outside: the regulators should ask themselves how far their enforcement reaches in case of a dispute, especially considering the many "failures" of China based companies on the SGX and Bursa. If you can't enforce, then there is no deterrent, the exchange will attract the wrong kind of people and fraud will happen.

I hope both exchanges will not introduce a dual class share structure. If founders really have a problem with the "one share, one vote" rule, they simply should not take outside money.

Friday, 9 September 2016

"Death Spiral" Convertibles should be banned

Quite a few news articles in Singapore regarding "death spiral" comvertibles lately.

An interesting look in the kitchen of a company (Advance Capital) helpng to structure and issue those bonds can be found here:

"Singapore-based firm starts fund to buy 'death spiral' convertibles"

Some snippets:

The firm and its fund specialises in convertible bonds that have been called "death spiral convertibles" because of their dilutive impact on the underlying shares. Under Advance Capital's programme, a listed company that is in need of funds will issue to Advance Capital convertible notes that are convertible into new shares of the company at a fixed discount to the current market price. Because the notes set the conversion discount, and not the price, some notes have the potential to create a runaway negative impact on the underlying stock as each round of conversion gets even more dilutive.

Advance Capital has previously made such deals with Attilan Group (the former Asiasons Capital), Elektromotive Group, Yuuzoo Corp, Cacola Furniture International and OLS Enterprise. Other firms that are active in such programmes include Value Capital Asset Management, which has made deals with Annica Holdings, ISR Capital, Magnus Energy Group and LionGold Corp.

Advance Capital does not intend to hold the convertible bonds to maturity - Mr Ng told The Business Times that the bonds typically carry only a nominal coupon that is insufficient to cover the credit risk of the issuer. Instead, Advance Capital prefers to convert the notes into shares, and to sell the shares within a few days of conversion for a profit.

David Webb warned about these instruments already eleven years ago, some snippets (emphasis mine):

Webb-site.com has been aware of the toxic convertibles scam for many years and have repeatedly warned the regulators about them in private, urging a regulatory ban. In our view, there can be no logical reason why a listed company would want to cede control to a third party over what amounts to a stream of future equity issues at deep discounts to market. The Listing Rules should be amended to prohibit listed companies from issuing convertible instruments which carry floating conversion prices. We have waited until now to compile this article because we wanted to conduct a comprehensive study of the actual results of these deals, which can each last several years, to prove how damaging they are.

SGX's reaction:

"The company must send shareholders a circular written in plain English and without overly legalistic jargon, before the shareholder vote," Mr Tan wrote. "In it, the company must make clear to shareholders how such a bond could cause a downward spiral of the share price and result in massive dilutions detrimental to investors. The company must state the 'floor', or minimum conversion price and the maximum number of shares which could be issued on exercise." Directors must also give an opinion that the issuance is in the best interest of the company and shareholders, and "explain to shareholders the alternative sources of financing considered before arriving at the decision to issue the convertibles". SGX may reject applications to issue such instruments if disclosures do not meet those minimum standards. Beyond ensuring adequate disclosures, however, SGX is not in the business of assessing the merits of such convertibles, Mr Tan stressed. The instruments are ultimately a source of capital, the appropriateness of which is a commercial decision best left to companies and shareholders, Mr Tan stressed.

And with that we wholeheartedly disagree. SGX can stress the need for plain English in circulars, but who reads them anyway? How much chance realistically has a minority shareholder to overturn a proposal to issue these toxic bonds if the proposal is supported by the Board of Directors?

SGX should heed the advice of David Webb and simply ban convertible bonds which carry a floating conversion price by amending the listing rules.

An interesting look in the kitchen of a company (Advance Capital) helpng to structure and issue those bonds can be found here:

"Singapore-based firm starts fund to buy 'death spiral' convertibles"

Some snippets:

The firm and its fund specialises in convertible bonds that have been called "death spiral convertibles" because of their dilutive impact on the underlying shares. Under Advance Capital's programme, a listed company that is in need of funds will issue to Advance Capital convertible notes that are convertible into new shares of the company at a fixed discount to the current market price. Because the notes set the conversion discount, and not the price, some notes have the potential to create a runaway negative impact on the underlying stock as each round of conversion gets even more dilutive.

Advance Capital has previously made such deals with Attilan Group (the former Asiasons Capital), Elektromotive Group, Yuuzoo Corp, Cacola Furniture International and OLS Enterprise. Other firms that are active in such programmes include Value Capital Asset Management, which has made deals with Annica Holdings, ISR Capital, Magnus Energy Group and LionGold Corp.

Advance Capital does not intend to hold the convertible bonds to maturity - Mr Ng told The Business Times that the bonds typically carry only a nominal coupon that is insufficient to cover the credit risk of the issuer. Instead, Advance Capital prefers to convert the notes into shares, and to sell the shares within a few days of conversion for a profit.

David Webb warned about these instruments already eleven years ago, some snippets (emphasis mine):

Webb-site.com has been aware of the toxic convertibles scam for many years and have repeatedly warned the regulators about them in private, urging a regulatory ban. In our view, there can be no logical reason why a listed company would want to cede control to a third party over what amounts to a stream of future equity issues at deep discounts to market. The Listing Rules should be amended to prohibit listed companies from issuing convertible instruments which carry floating conversion prices. We have waited until now to compile this article because we wanted to conduct a comprehensive study of the actual results of these deals, which can each last several years, to prove how damaging they are.

SGX's reaction:

"The company must send shareholders a circular written in plain English and without overly legalistic jargon, before the shareholder vote," Mr Tan wrote. "In it, the company must make clear to shareholders how such a bond could cause a downward spiral of the share price and result in massive dilutions detrimental to investors. The company must state the 'floor', or minimum conversion price and the maximum number of shares which could be issued on exercise." Directors must also give an opinion that the issuance is in the best interest of the company and shareholders, and "explain to shareholders the alternative sources of financing considered before arriving at the decision to issue the convertibles". SGX may reject applications to issue such instruments if disclosures do not meet those minimum standards. Beyond ensuring adequate disclosures, however, SGX is not in the business of assessing the merits of such convertibles, Mr Tan stressed. The instruments are ultimately a source of capital, the appropriateness of which is a commercial decision best left to companies and shareholders, Mr Tan stressed.

And with that we wholeheartedly disagree. SGX can stress the need for plain English in circulars, but who reads them anyway? How much chance realistically has a minority shareholder to overturn a proposal to issue these toxic bonds if the proposal is supported by the Board of Directors?

SGX should heed the advice of David Webb and simply ban convertible bonds which carry a floating conversion price by amending the listing rules.

Tuesday, 19 July 2016

SGX hiving off regulatory arm

One of the grouses against privatizing stock exchanges (like Bursa, SGX and HKEX) is the conflict of interest between the commercial and regulatory divisions.

The SGX has taken action on this matter, according to this article in the Business Times (Singapore):

SGX to hive off regulatory functions

Some snippets:

In a move welcomed by market watchers as long overdue, the Singapore Exchange (SGX) said on Monday that it is hiving off its regulatory arm from its commercial activities. A new company temporarily dubbed RegCo will be set up as an SGX subsidiary by the second half of next year. It will house SGX's current regulatory team of around 100 people. RegCo will be run by current SGX chief regulatory officer Tan Boon Gin, who reports directly to a board separate from the exchange. Central bank and regulator Monetary Authority of Singapore (MAS) will ensure SGX gives RegCo adequate resources for its duties.

Market players hailed SGX's move as a crucial one to resolve the long-running perception that the exchange was conflicted in having to regulate its clients, which include China-related S-chips and penny stocks that had been the focus of extreme speculative activity.

While some might still gripe that the regulatory unit is not totally independent of the SGX, others countered that RegCo's board, at least, will be separate and the majority of its members independent of SGX.

In a statement on Monday, MAS said the independence of the subsidiary will be an important factor for its success. It requires the chairman of RegCo as well as a majority of its directors to be independent of SGX and its subsidiaries. All directors also have to be independent of SGX-listed companies.

The SGX has taken action on this matter, according to this article in the Business Times (Singapore):

SGX to hive off regulatory functions

Some snippets:

In a move welcomed by market watchers as long overdue, the Singapore Exchange (SGX) said on Monday that it is hiving off its regulatory arm from its commercial activities. A new company temporarily dubbed RegCo will be set up as an SGX subsidiary by the second half of next year. It will house SGX's current regulatory team of around 100 people. RegCo will be run by current SGX chief regulatory officer Tan Boon Gin, who reports directly to a board separate from the exchange. Central bank and regulator Monetary Authority of Singapore (MAS) will ensure SGX gives RegCo adequate resources for its duties.

Market players hailed SGX's move as a crucial one to resolve the long-running perception that the exchange was conflicted in having to regulate its clients, which include China-related S-chips and penny stocks that had been the focus of extreme speculative activity.

While some might still gripe that the regulatory unit is not totally independent of the SGX, others countered that RegCo's board, at least, will be separate and the majority of its members independent of SGX.

In a statement on Monday, MAS said the independence of the subsidiary will be an important factor for its success. It requires the chairman of RegCo as well as a majority of its directors to be independent of SGX and its subsidiaries. All directors also have to be independent of SGX-listed companies.

Although the proof is in the pudding, this proposal sounds like a step in the right direction. Bursa Malaysia should consider to follow suit.

Saturday, 21 May 2016

Serious CG issues at SingPost

Very good article in The Star regarding corporate governance issues regarding a "government-linked logistics and e-commerce group".

We can safely assume that the company in question is non other than SGX listed SingPost.

The article centers around important issues like conflict of interest, independence of directors, “box-ticking corporate governance approach” and the important role of "public outrage".

The special audit report regarding the matter can be found here.

On one side, there is quite a lot of useful information to be found in this report about the process regarding the three acquisitions.

On the other side I think important details have been left out. For instance, a broad background of the three companies could have been given (some key numbers before and after the acquisition of each company plus the price for which they were acquired). The companies were acquired one, two and three years ago, so it would be interesting to know how they have performed since their acquisition.

Also, the money that Tay and his company earned through the transactions would have given more context: was it a tiny amount, or were millions of S$ involved?

And why did the three companies hire Tay's company as advisor, surely there must be hundreds of this kind of financial arrangers/advisors, was it mere coincidence?

It appears that the terms of reference for the special audit were too narrow to provide this kind of information, missing out on an opportunity to clear the air once and for all.

We can safely assume that the company in question is non other than SGX listed SingPost.

The article centers around important issues like conflict of interest, independence of directors, “box-ticking corporate governance approach” and the important role of "public outrage".

The special audit report regarding the matter can be found here.

On one side, there is quite a lot of useful information to be found in this report about the process regarding the three acquisitions.

On the other side I think important details have been left out. For instance, a broad background of the three companies could have been given (some key numbers before and after the acquisition of each company plus the price for which they were acquired). The companies were acquired one, two and three years ago, so it would be interesting to know how they have performed since their acquisition.

Also, the money that Tay and his company earned through the transactions would have given more context: was it a tiny amount, or were millions of S$ involved?

And why did the three companies hire Tay's company as advisor, surely there must be hundreds of this kind of financial arrangers/advisors, was it mere coincidence?

It appears that the terms of reference for the special audit were too narrow to provide this kind of information, missing out on an opportunity to clear the air once and for all.

Wednesday, 20 April 2016

SIAS to take legal action

Article in the Business Times (Singapore): "SIAS says it will take errant companies to court if need be".

Some snippets:

SIAS president and chief executive David Gerald told The Business Times: "We will take legal action if the company doesn't want to come to the table, refuses to see reason and continues to do wrong."

.... the SIAS chief said he felt it was important to let SIAS members and retail investors know that they have the option of joining the association in a representative action - similar in vein to class-action suits filed in other jurisdictions - as not many investors are aware that such actions can be pursued here. "Investors must know they are protected," he said. "And I have been advised by our lawyers that SIAS can represent aggrieved shareholders. We can even set up a litigation fund, which minorities contribute to, even if they may not be involved in the legal action, to support the principle."

Mr Gerald took pains to stress, however, that while a representative action is an option for minorities, it should be their last one. "I sincerely hope we do not see the day when we launch a class-action suit against a company. I believe in resolving things in the boardroom, not the courtroom, in the interest of all parties."

Although I don't always agree with the actions of the SIAS, I fully support the above reasoning. It is very hard for minority shareholders to group together, while taking action individually doesn't make sense at all because of the costs involved (unless it involves a relatively large minority shareholder, like a fund).

SIAS and MSWG are ideal platforms to organize legal action for minority investors that have been disadvantaged.

Some snippets:

SIAS president and chief executive David Gerald told The Business Times: "We will take legal action if the company doesn't want to come to the table, refuses to see reason and continues to do wrong."

.... the SIAS chief said he felt it was important to let SIAS members and retail investors know that they have the option of joining the association in a representative action - similar in vein to class-action suits filed in other jurisdictions - as not many investors are aware that such actions can be pursued here. "Investors must know they are protected," he said. "And I have been advised by our lawyers that SIAS can represent aggrieved shareholders. We can even set up a litigation fund, which minorities contribute to, even if they may not be involved in the legal action, to support the principle."

Mr Gerald took pains to stress, however, that while a representative action is an option for minorities, it should be their last one. "I sincerely hope we do not see the day when we launch a class-action suit against a company. I believe in resolving things in the boardroom, not the courtroom, in the interest of all parties."

Although I don't always agree with the actions of the SIAS, I fully support the above reasoning. It is very hard for minority shareholders to group together, while taking action individually doesn't make sense at all because of the costs involved (unless it involves a relatively large minority shareholder, like a fund).

SIAS and MSWG are ideal platforms to organize legal action for minority investors that have been disadvantaged.

Sunday, 17 April 2016

Linc Energy: from "20 Trillion" to Administration in 3 years time

Linc Energy was once the darling of the speculators. When the company was still listed on the ASX, valuations of 20 Trillion were mentioned.

.... two independent consultants estimated there was an ‘‘unrisked prospective resource’’ of up to 223 billion barrels of oil equivalent in three shale formations within its 100 per cent-held Arckaringa exploration permits.

Media outlets including the Adelaide Advertiser appear to have multiplied the resource estimate by the prevailing oil price - above $US95 a barrel - to arrive at the $20 trillion figure.

Even for Linc Energy, that sounded a "bit" too rich, so they added:

‘‘It’s a multi-billion barrel opportunity, and that’s a good news story. OK it’s not $20 trillion. But 3, 4, 5 billion barrel resources are virtually unheard of these days, so even stressing this number down to the minimum number the experts stress it down to, it’s still a big story.’’

The company subsequently dumped the ASX for the SGX.

Quite a scoop for the latter, but if they are still happy with their "catch" remains doubtful, since Linc Energy went into voluntarily administration last week:

Linc, which once boasted a market value of $2 billion when listed in Australia, was worth $US15 million when its Singapore-listed shares last traded on March 24. Former Australian listed market darling Linc Energy has entered voluntary administration with the oil- and gas-focused company buckling under an ongoing debt restructure and recapitalisation.

The above story shows the danger of those "consultants", especially the kind who come up with rosy valuations, without putting in one cent of their own money. Even Genting apparently believed in the story, they owned 10% of the shares of Linc. It also shows how quickly the fortunes of highly indebted commodity companies can change.

.... two independent consultants estimated there was an ‘‘unrisked prospective resource’’ of up to 223 billion barrels of oil equivalent in three shale formations within its 100 per cent-held Arckaringa exploration permits.

Media outlets including the Adelaide Advertiser appear to have multiplied the resource estimate by the prevailing oil price - above $US95 a barrel - to arrive at the $20 trillion figure.

Even for Linc Energy, that sounded a "bit" too rich, so they added:

‘‘It’s a multi-billion barrel opportunity, and that’s a good news story. OK it’s not $20 trillion. But 3, 4, 5 billion barrel resources are virtually unheard of these days, so even stressing this number down to the minimum number the experts stress it down to, it’s still a big story.’’

The company subsequently dumped the ASX for the SGX.

Quite a scoop for the latter, but if they are still happy with their "catch" remains doubtful, since Linc Energy went into voluntarily administration last week:

Linc, which once boasted a market value of $2 billion when listed in Australia, was worth $US15 million when its Singapore-listed shares last traded on March 24. Former Australian listed market darling Linc Energy has entered voluntary administration with the oil- and gas-focused company buckling under an ongoing debt restructure and recapitalisation.

The above story shows the danger of those "consultants", especially the kind who come up with rosy valuations, without putting in one cent of their own money. Even Genting apparently believed in the story, they owned 10% of the shares of Linc. It also shows how quickly the fortunes of highly indebted commodity companies can change.

Saturday, 9 January 2016

Rating agencies are mostly useless

I have written about rating agencies before, in not too positive terms, being hopelessly slow and conflicted.

Standard & Poor's has added further to this impression by downgrading Noble Group's rating to junk only now:

"S&P lowered Noble Group’s rating to BB+ from BBB- and placed it on watch for further possible downgrade, the ratings company said in a statement on Thursday, following a similar move by Moody’s Investors Service in late December. Noble’s dollar bonds due in 2020 dropped to a record low of 54.78 cents on the dollar, according to prices compiled by Bloomberg."

Iceberg Research, the company that started to roll the ball in this case almost one full year ago, wrote this about the downgrade:

S&P has downgraded Noble Group to junk today, following a similar move by Moody’s.

The downgrade validates one of our main arguments against Noble: this company has never been investment grade. In fact, the question is why did it take so long when it was clear that Noble has been bleeding cash for years, and after we showed that profitability was supported by dubious mark-to-market?

The decision will have an important impact on Noble’s liquidity and the perception of its creditors. This further complicates the refinancing of its debt. Noble’s annual results will soon be audited and we doubt that this time, EY will take more legal risks when they sign off on the accounts.

The financial manipulations were conducted to artificially preserve the investment grade rating. The accounting illusion is now over. With a share price down 71% since our first report, and strong doubts over the balance sheet, Noble is facing an even more acute crisis. The group is slowly moving toward bankruptcy.

Most of our arguments on Noble’s accounting have already become facts. This management has completely lost credibility. It is urgent for Noble’s stakeholders to replace Mr. Elman and Mr. Alireza before the company sinks with them.

Standard & Poor's has added further to this impression by downgrading Noble Group's rating to junk only now:

"S&P lowered Noble Group’s rating to BB+ from BBB- and placed it on watch for further possible downgrade, the ratings company said in a statement on Thursday, following a similar move by Moody’s Investors Service in late December. Noble’s dollar bonds due in 2020 dropped to a record low of 54.78 cents on the dollar, according to prices compiled by Bloomberg."

Iceberg Research, the company that started to roll the ball in this case almost one full year ago, wrote this about the downgrade:

S&P has downgraded Noble Group to junk today, following a similar move by Moody’s.

The downgrade validates one of our main arguments against Noble: this company has never been investment grade. In fact, the question is why did it take so long when it was clear that Noble has been bleeding cash for years, and after we showed that profitability was supported by dubious mark-to-market?

The decision will have an important impact on Noble’s liquidity and the perception of its creditors. This further complicates the refinancing of its debt. Noble’s annual results will soon be audited and we doubt that this time, EY will take more legal risks when they sign off on the accounts.

The financial manipulations were conducted to artificially preserve the investment grade rating. The accounting illusion is now over. With a share price down 71% since our first report, and strong doubts over the balance sheet, Noble is facing an even more acute crisis. The group is slowly moving toward bankruptcy.

Most of our arguments on Noble’s accounting have already become facts. This management has completely lost credibility. It is urgent for Noble’s stakeholders to replace Mr. Elman and Mr. Alireza before the company sinks with them.

Monday, 21 September 2015

Limited ads on SGX website

A rather terse letter from the SGX to the editor of Straits Times (Singapore) regarding the SGX placing advertisements on their website, something I have written about already in 2013.

A few snippets with some comments by me:

"Online advertising is not unique to SGX among exchanges globally."

But that does not mean it is good. There are also many exchanges that do not publish advertisements (or only some, which are related and endorsed), like Bursa.

Many other exchanges are also public companies (which I am strongly against, due to the inherent conflict of interest), which might explain (part of) it, trying to maximize (or at least increase) profits.

The issue for me is that advertisements on the SGX website might be interpreted by viewers as being endorsed by the SGX, which is not the case. And for that reason alone, the SGX should not publish advertisements, in my opinion.

"SGX continually reviews the advertising categories and advertisers and blocks those not deemed fit for purpose."

In my posting an advertisement was not blocked that involved a company (Infinity Treasures) that is listed on the MAS Investor Alert List. Was that company "deemed fit for purpose"?

"Meanwhile, we are in the process of reviewing our website interface, having taken in constructive public feedback that it could be improved."

At least some good news, I have been very critical of SGX's website (Bursa's is so much better, faster, more easy to use, etc.), looking forward to the new website.

A few snippets with some comments by me:

"Online advertising is not unique to SGX among exchanges globally."

But that does not mean it is good. There are also many exchanges that do not publish advertisements (or only some, which are related and endorsed), like Bursa.

Many other exchanges are also public companies (which I am strongly against, due to the inherent conflict of interest), which might explain (part of) it, trying to maximize (or at least increase) profits.

The issue for me is that advertisements on the SGX website might be interpreted by viewers as being endorsed by the SGX, which is not the case. And for that reason alone, the SGX should not publish advertisements, in my opinion.

"SGX continually reviews the advertising categories and advertisers and blocks those not deemed fit for purpose."

In my posting an advertisement was not blocked that involved a company (Infinity Treasures) that is listed on the MAS Investor Alert List. Was that company "deemed fit for purpose"?

"Meanwhile, we are in the process of reviewing our website interface, having taken in constructive public feedback that it could be improved."

At least some good news, I have been very critical of SGX's website (Bursa's is so much better, faster, more easy to use, etc.), looking forward to the new website.

Friday, 21 August 2015

Silverlake Axis down 24%, suspended, after damning report

Trading in Singapore listed, Malaysia based, software solution provider Silverlake Axis was halted today after the share plunged 24%, as reported by The Edge.

The reason for the plunge and the trading halt is the following anonymous report:

"The Unbelievable Financial Alchemy of Silverlake Axis"

It is a rather comprehensive report with quite a lot of detail. I leave it to the readers to draw their own conclusions.

A bit more background about the company and its founder can be found in two recent articles in The Star, here and here. From the last article, one worrisome sentence:

"But investors find it hard to comprehend technology-based companies and even in the region, where Singapore-listed Silverlake Axis has a S$3.19bil market capitalisation, and where the bulk of its business derives from, many do not understand the company."

What now is needed from Silverlake Axis is a comprehensive, blow-by-blow, answer on all allegations in a very short time, preferably over the weekend. A flat denial, a superfluous answer or an attempt to shoot the messenger will simply not do (I guess Noble Group will agree with that, they have tried them all before).

Silverlake Axis should also be able to come up with a quick answer since this report does not come as a surprise. Rumours have been flying regarding this company for quite some time (I was aware of them), witnessed for instance by this article or this posting. In other words, the company was warned and should be prepared.

For Malaysia, it is another blow to its decreasing credibility.

First of all, there are simply too many scandals recently.

Secondly, corruption (one of the country's largest problems) is mentioned in the report as a possibility:

The corruption is not actually proven (that would be very hard to do for an outsider), but in the main report itself there is clearly more detail given than the above.

The reason for the plunge and the trading halt is the following anonymous report:

"The Unbelievable Financial Alchemy of Silverlake Axis"

It is a rather comprehensive report with quite a lot of detail. I leave it to the readers to draw their own conclusions.

A bit more background about the company and its founder can be found in two recent articles in The Star, here and here. From the last article, one worrisome sentence:

"But investors find it hard to comprehend technology-based companies and even in the region, where Singapore-listed Silverlake Axis has a S$3.19bil market capitalisation, and where the bulk of its business derives from, many do not understand the company."

What now is needed from Silverlake Axis is a comprehensive, blow-by-blow, answer on all allegations in a very short time, preferably over the weekend. A flat denial, a superfluous answer or an attempt to shoot the messenger will simply not do (I guess Noble Group will agree with that, they have tried them all before).

Silverlake Axis should also be able to come up with a quick answer since this report does not come as a surprise. Rumours have been flying regarding this company for quite some time (I was aware of them), witnessed for instance by this article or this posting. In other words, the company was warned and should be prepared.

For Malaysia, it is another blow to its decreasing credibility.

First of all, there are simply too many scandals recently.

Secondly, corruption (one of the country's largest problems) is mentioned in the report as a possibility:

The corruption is not actually proven (that would be very hard to do for an outsider), but in the main report itself there is clearly more detail given than the above.

Monday, 17 August 2015

Unethical companies

The Norges Bank has a list with exclusions in which the Norwegian state fund is not allowed to invest in, based on ethical considerations.

The Guidelines for observation and exclusion from the Government Pension Fund Global can be found here.

More fund managers are looking these days at CSR (Corporate social responsibility) issues and the Norwegian fund is a very large fund, so this list will most likely become more important over time.

On the list of about 65 companies there are several Malaysian companies, the latest additions being Genting and IJM, both because of their plantations. The Malaysian companies:

From Singapore:

The Guidelines for observation and exclusion from the Government Pension Fund Global can be found here.

More fund managers are looking these days at CSR (Corporate social responsibility) issues and the Norwegian fund is a very large fund, so this list will most likely become more important over time.

On the list of about 65 companies there are several Malaysian companies, the latest additions being Genting and IJM, both because of their plantations. The Malaysian companies:

- British American Tobacco Bhd (Production of tobacco)

- IJM Corp Bhd (Severe environmental damages)

- Genting Bhd (Severe environmental damages)

- WTK Holdings Bhd (Severe environmental damages)

- Ta Ann Holdings Bhd (Severe environmental damages)

- Lingui Development Bhd (Severe environmental damages)

From Singapore:

- Singapore Technologies Engineering (Anti-personnel land mines)

Friday, 3 July 2015

JES: will the CEO take action against her father?

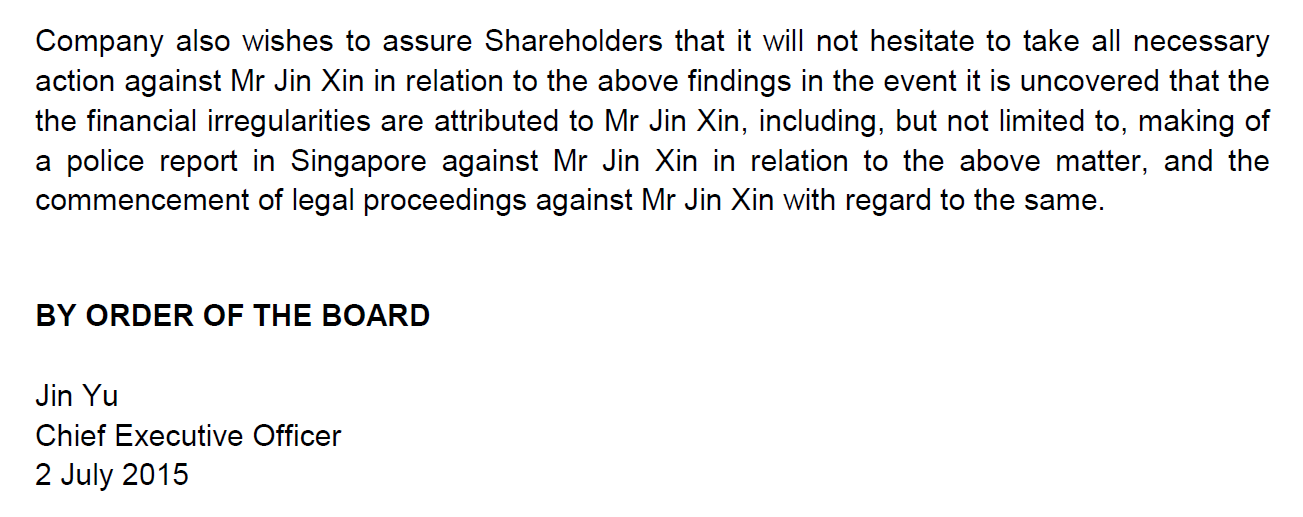

In Singapore SGX listed (China based) company JES announced that an employee of the company has run away with the company's account books, chequebooks and financial seals, delaying the probe into financial irregularities of Mr. Jin Xin.

Apparently the books were not digitally stored in the "cloud", in which case a simple back-up would have been enough to preserve the data.

The company promised to take necessary action against Jin Xin:

Strong words by the CEO, and certainly a great assurance for the beleaguered shareholders (JES's shares are suspended for four months already) that appropriate action will be taken, until one realizes that Jin Yu is actually the daughter of Jin Xin.

From the Straits Times:

A female employee has delayed an investigation into dubious payments to the former boss of Chinese shipbuilder JES International by "absconding" with the company's books.

JES International has begun legal proceedings in China against the woman, administrative officer Ju Li Li, to recover the documents.

After Mr Jin Xin, the group's former chief executive and chairman, resigned in March, Ms Ju "absconded" with the group's administration records and seals of all its Chinese subsidiaries, JES told the Singapore Exchange last night.

JES, now helmed by Mr Jin's daughter, Ms Audrey Jin Yu, said it had intended to investigate its financials after uncovering possible irregularities during a periodic review. These included "questionable transactions" between the group and companies in which Mr Jin's interests were not declared, JES said.

But "the financial records of the group, including account books, chequebooks and financial seals, had been removed... by relatives of Mr Jin", JES said in its filing.

Mr Jin, who resigned from his post as executive director due to "health issues" on May 25, is not the only one to have quit.

On May 15, JES appealed to the Singapore bourse to extend its deadline for announcing first-quarter earnings, citing "a severe shortage of manpower" after half of its finance department resigned.

JES assured shareholders yesterday that if the books are recovered and Mr Jin is found at fault, "necessary action" would be taken. Trading of JES shares has been suspended since March 4. The shares last traded at 2.6 Singapore cents.

Apparently the books were not digitally stored in the "cloud", in which case a simple back-up would have been enough to preserve the data.

The company promised to take necessary action against Jin Xin:

Strong words by the CEO, and certainly a great assurance for the beleaguered shareholders (JES's shares are suspended for four months already) that appropriate action will be taken, until one realizes that Jin Yu is actually the daughter of Jin Xin.

From the Straits Times:

A female employee has delayed an investigation into dubious payments to the former boss of Chinese shipbuilder JES International by "absconding" with the company's books.

JES International has begun legal proceedings in China against the woman, administrative officer Ju Li Li, to recover the documents.

After Mr Jin Xin, the group's former chief executive and chairman, resigned in March, Ms Ju "absconded" with the group's administration records and seals of all its Chinese subsidiaries, JES told the Singapore Exchange last night.

JES, now helmed by Mr Jin's daughter, Ms Audrey Jin Yu, said it had intended to investigate its financials after uncovering possible irregularities during a periodic review. These included "questionable transactions" between the group and companies in which Mr Jin's interests were not declared, JES said.

But "the financial records of the group, including account books, chequebooks and financial seals, had been removed... by relatives of Mr Jin", JES said in its filing.

Mr Jin, who resigned from his post as executive director due to "health issues" on May 25, is not the only one to have quit.

On May 15, JES appealed to the Singapore bourse to extend its deadline for announcing first-quarter earnings, citing "a severe shortage of manpower" after half of its finance department resigned.

JES assured shareholders yesterday that if the books are recovered and Mr Jin is found at fault, "necessary action" would be taken. Trading of JES shares has been suspended since March 4. The shares last traded at 2.6 Singapore cents.

Friday, 1 May 2015

Bursa limits information to 5 years ONLY? (2)

MSWG comments on the same issue in their newsletter for April 30, 2015:

"On the capital market scene, recently, to our surprise, we learnt of a significant change in the provision of statistics and information pertaining to public listed companies (PLCs) on Bursa Malaysia website.

We have received complaints from retail investors and noticed that statistics and information including company announcements, quarterly financial results and annual reports were only available on the Bursa Malaysia website for 5 years. Hitherto, these information were generally made available for 10 years. We do not know why Bursa has taken this step to truncate information available to the public to only 5 years. In addition, no announcement was made on such a change.

Also, we believe this new development is somewhat regressive. It is always preferable for investors to have longer period of 10 years’ statistics including historical data and announcements at a one-stop centre to enable investors to carry out meaningful research. Particularly, if they need to do a time-series analysis which requires longer historical data.

We urge Bursa to reconsider providing these important statistics for the consumption of the general investing public who relies on reliable and up-to-date information in order to develop a more vibrant retail investors’ market."

First of all great that MSWG puts pressure on Bursa to reconsider the change.

I am also rather surprised, I would have thought that MSWG would have been kept in the loop of radical changes like this, but apparently not.

As far as I remember, Bursa started with their platform in (probably, I do remember some material from before 2000) 1999, and simply kept all announcements ever made.

In other words a great archive of all kind of information: financial results, IPO documents, shareholder changes of directors and major shareholders, related party transactions, etc.

I have been critical of Bursa on many occasions (mostly on enforcement related matters), but I have praised their website, for instance here:

"Despite having an otherwise excellent announcement website (I can't stress this enough, it is much better than all other announcements websites that I frequent), there is always room for improvement I guess."

If Bursa restricts the announcements to only the last five years, then I am afraid I have to take back my compliment.

The HKEX for instance gives information starting 1999:

SGX seems to be the worst of the three. They only offer announcements since 2010, also the user interface is confusing (their last update made things even worse), at least, that is my opinion. In addition to that, they even make money on advertisements through Googleads, which I think they really should not do (users might mistakenly think that the companies featured in the ads are supported by SGX, which they aren't). SGX is making enough money as an exchange, they don't need this extra source of income.

"On the capital market scene, recently, to our surprise, we learnt of a significant change in the provision of statistics and information pertaining to public listed companies (PLCs) on Bursa Malaysia website.

We have received complaints from retail investors and noticed that statistics and information including company announcements, quarterly financial results and annual reports were only available on the Bursa Malaysia website for 5 years. Hitherto, these information were generally made available for 10 years. We do not know why Bursa has taken this step to truncate information available to the public to only 5 years. In addition, no announcement was made on such a change.

Also, we believe this new development is somewhat regressive. It is always preferable for investors to have longer period of 10 years’ statistics including historical data and announcements at a one-stop centre to enable investors to carry out meaningful research. Particularly, if they need to do a time-series analysis which requires longer historical data.

We urge Bursa to reconsider providing these important statistics for the consumption of the general investing public who relies on reliable and up-to-date information in order to develop a more vibrant retail investors’ market."

First of all great that MSWG puts pressure on Bursa to reconsider the change.

I am also rather surprised, I would have thought that MSWG would have been kept in the loop of radical changes like this, but apparently not.

As far as I remember, Bursa started with their platform in (probably, I do remember some material from before 2000) 1999, and simply kept all announcements ever made.

In other words a great archive of all kind of information: financial results, IPO documents, shareholder changes of directors and major shareholders, related party transactions, etc.

I have been critical of Bursa on many occasions (mostly on enforcement related matters), but I have praised their website, for instance here:

"Despite having an otherwise excellent announcement website (I can't stress this enough, it is much better than all other announcements websites that I frequent), there is always room for improvement I guess."

If Bursa restricts the announcements to only the last five years, then I am afraid I have to take back my compliment.

The HKEX for instance gives information starting 1999:

SGX seems to be the worst of the three. They only offer announcements since 2010, also the user interface is confusing (their last update made things even worse), at least, that is my opinion. In addition to that, they even make money on advertisements through Googleads, which I think they really should not do (users might mistakenly think that the companies featured in the ads are supported by SGX, which they aren't). SGX is making enough money as an exchange, they don't need this extra source of income.

Subscribe to:

Posts (Atom)